Home » Kevin Vitali Massachusetts REALTORS-Real Estate Blog » Buying A House » What Does A Fed Rate Hike Mean For Home Mortgages?

What Does A Fed Rate Hike Mean For Home Mortgages?

First, let’s just get it out there….. The Federal Reserve does not set mortgage rates.

First, let’s just get it out there….. The Federal Reserve does not set mortgage rates.

Yet, nothing puts fear in homebuyers fervently looking for homes and hearing about a pending Fed Hike Rate. Many hear about the Federal Reserve increasing rates and assume it is a 1:1 correlation to interest rates on home loans rising.

Meaning, if the Feds hike the rate by 3/4 of a point, interest rates for home mortgage will also rise 3/4 of a point.

Homebuyers already feeling the pinch of massive increases in mortgage rates cringed as they heard the Feds were raising interest rates again in July. The buyers have sat and watched their buying power get eaten up by earlier interest rate hikes in the beginning half of 2022.

But, as homebuyers heard the news of the rate hike, mortgage rates remained relatively unchanged.

While a Fed Hike Rate Hike does not directly affect interest rates on home mortgages, it definitely has a large impact on home loan interest rates, but not like you think.

What Does A Fed Rate Hike Mean?

The Federal Reserve Bank uses the Federal Interest Rate to control the supply of money. The Federal Interest Rate controls the commercial interest rate charged between banks for short term loans.

The Federal Reserve Uses Rate Hikes and Cuts To Control The Economy

In the case of a Fed Interest Rate Hike, the cost to borrow money is higher and the hope is people save money and not spend it. As consumers spends less, it lightens the burden on the supply and demand. Hopefully it will cause prices to stabilize or fall.

When the Feds cut rates, it is in hopes that in encourages the public to spend money and get the economy rolling.

Rate hikes and cuts are like a faucet to get more money flowing or restrict the flow. It is one of the few tools the Federal Bank has to control the economy.

The July 2022 rate hike was in hopes of slowing inflation and avoiding a recession.

How Does The Fed Rate Hike Affect Mortgage Interest Rates?

As I said in the beginning of this article, the Federal Reserve Banks don’t control mortgage interest rates directly.

Though indirectly, a Fed Rate Hike will affect interest rates for mortgages.

First, realize that the interest rate for home loans is controlled by mortgage backed securities. Similar to a bond, they are bundled home loans purchased by institutional investors. Mortgage backed securities are an independent market and rise and fall on their own.

Not to say, that the rise in the Federal interest rate isn’t one of the factors that impact mortgage backed securites.

Fed Hike Rates Have A Psychological Impact On Investors

The impact a rate hike (or cut) has from the Feds is more psychological than anything. When the Federal Bank raises the Federal Interest Rate, investors are looking for other signals about how the economy is doing.

A change in the Federal interest rate is just one of many factors investors use to determine how to invest their money. Investors try to look at the overall health of the economy. Monetary policy is just one factor.

What the Fed has to say after the hike or cut, is almost as important as the change itself. Investors are hoping to get a glimpse of the economic future.

When investors feel that the economy is doing poorly or predicts a failing economy is around the corner, then mortgage backed securities are a safe place to park their money. They get a decent return on a low risk investment.

As investors flood to mortgage backed securities, the interest rate drops because there is a greater demand than supply. But as investors see a flourishing economy, the rate for mortgage back securities rise to attract investors who feel they may have better options.

The Federal Bank May Purchase or Sell Assets To Control the Flow

The housing economy is certainly an important segment for the overall economy.

The Federal Reserve will also buy and sell mortgage backed securities to help control the economy. During the pandemic, the Fed started purchasing bonds and securities in hopes of spurring the economy.

The result from the purchases, during the beginning part of the pandemic, was a drop in mortgage interest rates.

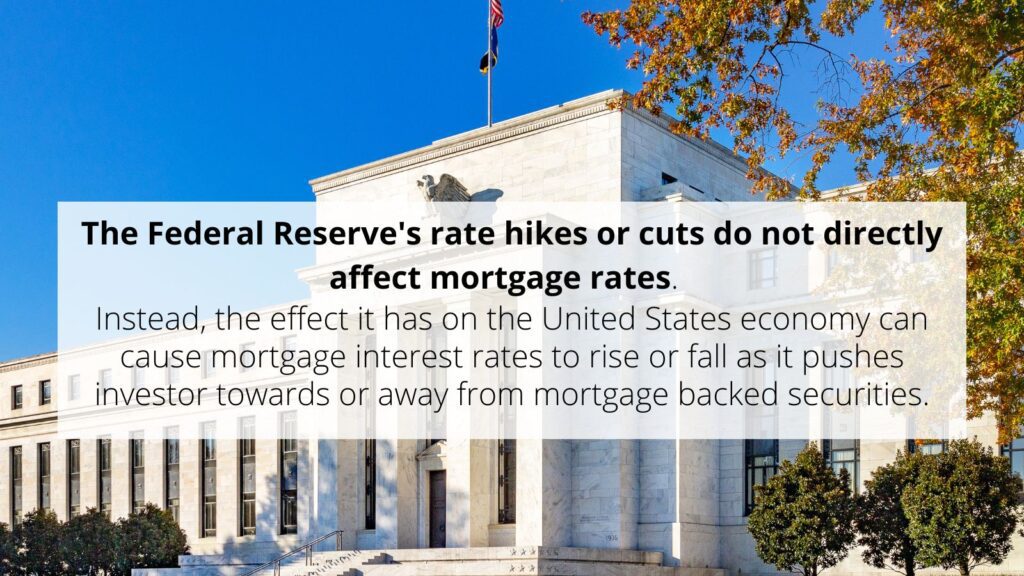

The Federal Reserve’s rate hikes or cuts do not directly affect mortgage rates. Instead, the effect it has on the United States economy can cause mortgage interest rates to rise or fall as it pushes investor towards or away from mortgage backed securities.

July 2022’s Federal Reserves Announcement

July 2022 was the fourth interest rate hike since the beginning of the year. Each subsequent rate hike announcement has had a smaller and smaller impact on mortgage rates.

Overall, investors had already drastically reacted to the previous rate hikes and have already formed their decisions for the future.

The July interest rate hike by the Fed’s was a big one, .75 basis points. Yet, mortgage interest rates have remained relatively unchanged. As a matter of fact, interest rates on home loans dropped shortly after the announcement.

Many investors feel by definition we are in a recession, even though the administration has not called it yet. That has had investors turning towards mortgage backed securities as they wait out any volatility in the stock market.

And as I pointed out earlier, as a growing group of investors seeks out mortgage backed securities, interest rates on home loans will drop.

What Does The Latest Fed Rate Hike Mean For Homebuyers?

Homebuyers are already impacted by huge appreciation of houses over the past several years. Combine that with drastic increases in mortgage rates and you will see homebuyers buying power eaten up.

What do I mean? A homebuyer that was pre-approved for $600k back in January is probably looking at a $120k drop in their max pre-approval. That’s the difference of $660k to $480k.

Of course, no borrower is the same and there are other factors that go into qualifying for a mortgage, such as debt to income ratio and a borrowers credit score.

I always tell buyers the time to buy a home is when it’s time to buy a home. Don’t try to time the market. If the timing is right to buy now, then buy.

For some markets, across the US, you may see a drop in home prices. Others will see appreciations slow drastically or even flatten.

The remainder of 2022 and the beginning of 2023 will see the Massachusetts real estate market flatten out.

It will no longer be a market that favors the seller and will become a neutral market. This will get rid of of the chaos buyers have been experiencing the past couple of years.

Homebuyers should also consider that if you wait on the sidelines, homes may still appreciate, at a much slower rate and interest rates could go up. If you bought at the peak of the market in 2007, even though you saw some double-digit depreciation over the next few years, today you are sitting pretty with a ton of equity in your home.

Buy for the long haul.

How Will The Fed Rate Hike Effect Sellers?

Let’s face it. Sellers have had it pretty darn easy the past few years. Open house flooded with buyers, houses sold in a week, multiple offers over asking, etc…

But hyper appreciation of homes combined with much higher interest rates will make buyers hesitant and even push some out of the market.

In the whole scheme of things, this is only a small snippet of time driven by market conditions.

Today, in the Haverhill MA Real Estate market we are seeing days on market increase and home sitting on the market longer and more properties with price changes and much steeper price changes. But, the market is still very strong.

For Massachusetts home sellers, the market will slowly start to soften.

Adjust your expectations and realize you will have to go back to the basics of selling a home. This includes improving curb appeal, preparing your home, understanding pricing principles and more…

Summary

Federal Reserves rate hikes don’t impact mortgage rates directly, but can certainly influence how investors see the market and how they react as they go in and out of mortgage backed securities

There will definitely be some unpredictability coming up in interest rates for home mortgages, but don’t think it is solely because of the Fed rate hikes. Look towards the overall economy in general.

Other Massachusetts Real Estate Resources

- Is the market turning towards a buyer’s market? Bill Gassett explains how to identify a buyer’s market. Signs to look for are increased days on market, price decreases on current inventory, and more.

- During my real estate career as a Massachusetts real estate agent, I am constantly seeing buyers and sellers trying to time the real estate market. Paul Sian gives some great advice on trying to time the real estate market and why it could be a big mistake.

- Sometimes it can be difficult to sell a house. And, it may have nothing to do with the house itself. Vicki Moore covers 6 reasons your house may not sell.